Businesses express cautious optimism for this festive season

Different business strategies have given new meaning to Black Friday in Malta, bringing more positives overall for the whole month of November rather than during the specific day known as Black Friday.

A survey concluded by the Malta Chamber of SMEs has confirmed that this year many businesses decided to extend their offers beyond just the day of Black Friday and while this led to a calmer 26th of November – Black Friday, it also gave businesses a strong November and results which left the majority satisfied overall.

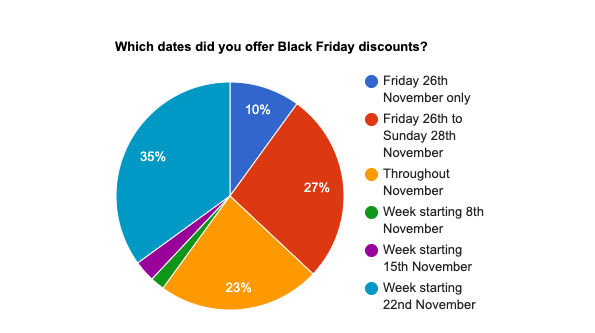

In terms of the period during which the Black Friday offers were available, most popular was Black Friday Week starting the 22nd of November with 35% of businesses opting for this option. This was followed by the ‘Black Friday Weekend’ at 27% and closely followed by those opting to run offers throughout the month of November at 23%.

Extending the offers on a longer period resulted in a successful strategy for most businesses. Businesses wanted to avoid overcrowding and queues because of Covid. In addition, given the dire situation all businesses are facing in terms of human resources, this strategy helped them keep up with the increased demands, while also maintaining the same level of customer service.

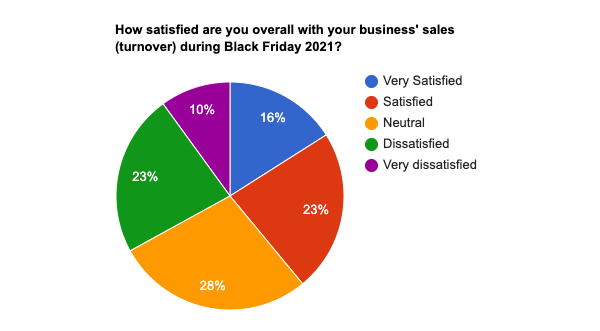

As for the results related to the level of business, highest scoring were businesses that expressed their satisfaction (23%) or high degree of satisfaction (16%) with the level of business generated thanks to Black Friday. Together these made 39% of respondents.

The most common sectors to be found here are household goods, electronics, beauty and personal care services as well as education and training.

On average, business increased by around 30% over the same period last year for businesses that performed well. When asked what they attributed this result to, most mentioned their own effective marketing strategies, increased investment in their online presence, more offers made available as well as increased consumer confidence. They however acknowledged that the bad weather during the Black Friday Week might have affected them negatively.

Those which expressed their dissatisfaction (23%) or a high degree of dissatisfaction (10%), together 33%, mainly came from sectors not normally associated with Black Friday and those predominantly selling essential items.

On average, business here decreased by around 25% over the same period last year for businesses that performed poorly. Bad weather conditions, competition from overseas and consumers being cautious with their spending were the most common reasons quoted, together with the complications related to international shipping which did not result in ideal stock complement.

Malta Chamber of SMEs CEO, Abigail Agius Mamo, said that these results leave room for optimism. Malta is surely on the road to recovery, albeit the pace of recovery being a slow one. Businesses need to recover at a faster pace to start making up for the losses sustained since the start of the pandemic, a steady recovery is however is the best one can hope for.’

It was noted that the percentage of businesses that chose not to participate in the Black Friday campaigns, because they believe that focusing on selling during Christmas and New Year is more important, continues to decrease year on year and in fact this year the percentage is a marginal one.

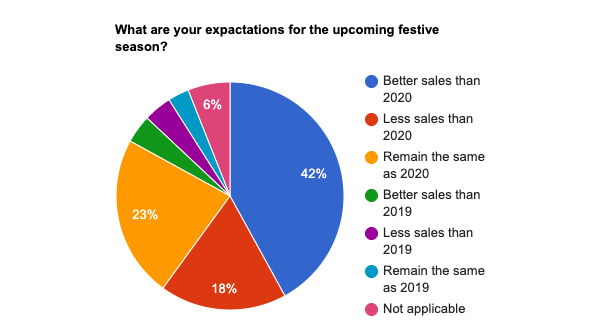

The Chamber of SMEs also asked businesses for their expectations for this year’s festive season. The majority, at 42% expect to be in a better than 2020, followed by 23% that believe that sales levels will be comparable with 2020 levels. 18% feel that they might fare worse than last year and 11% of businesses feel that on the other hand this festive season will be closer to 2019 levels.

‘The Chamber of SMEs feels that businesses are more cautious in their optimism, compared to weeks and months ago. Malta is highly dependent on the functioning of foreign markets, making it very sensitive to Covid developments in other countries and on an international level. Businesses are however looking forward to give their best for a successful festive season’ concluded Ms Agius Mamo.